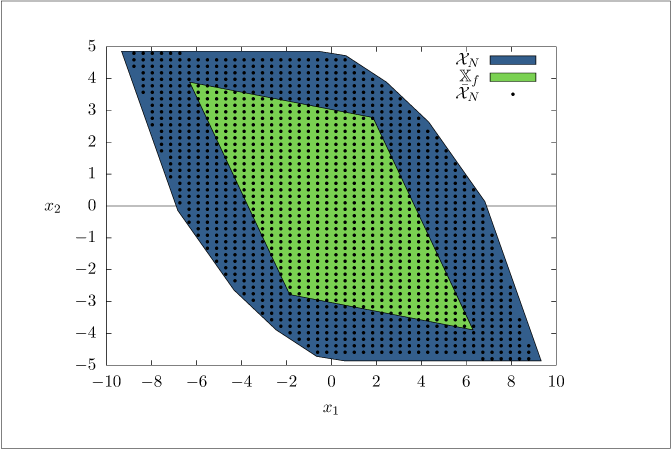

The region of attraction for terminal constraint x(N) \in \mathbb {X}_f and terminal penalty V_f(x)=(1/2)x' \Pi x and the estimate of \bar {\mathcal {X}}_N for Exercise \ref {exer:NoTerminal}.

# [Xk, Uk, phi, status, matrices] = linearmpc(model, constraint, penalty, terminal, [matrices])## Solves the following optimization problem:## N-1# min sum [ 1/2(x_k' Q x_k + u_k' R u_k ) ] + 1/2(x_N' P x_n)# u_k k=1## s.t x_k+1 = A x_k + B u_k# G x_k + H u_k <= psi# A_f x_N <= b_f## Linear time-invariant MPC.## Input 'model' has the following fields:# - A: A matrix for system.# - B: B matrix for system.# - N: horizon length in number of stemps.# - x0: initial state of system.## Input 'constraint' has the following fields:# - G: G matrix for constraints.# - H: G matrix for constraints.# - psi: psi vector for constraints.# Either all or none must be specified.## Input 'penalty' has the following fields:# - Q: Penalty matricies for state.# - R: Penalty matrix for input.# - P: Terminal penalty matrix.## Input terminal can be a vector of length x to specify a terminal equality# constraint, or a struct with fields A and b (corresponding to A_f and b_f in# the optimization given above).## The final output matrices is a struct with fields H, f, Alt, blt, Aeq, beq,# lb, and ub that define the QP formulation. If these are supplied in a struct# as a fifth argument, only the initial condition model.x0 is updated, and the# matrices are passed directly to the QP solver. This can save a lot of time if# you're solving the same problem over and over but with different initial# conditions. Note that minimal error checking is done# Check arguments.importnumpyasnpfromscipyimportsparsefromscipy.optimizeimportminimizeimportwarningsdeflinearmpc(model,constraint,penalty,terminal,matrices=None):""" Solves linear time-invariant MPC optimization problem. Args: model: dict with fields A, B, N, x0 constraint: dict with fields G, H, psi penalty: dict with fields Q, R, P terminal: vector or dict with fields A, b matrices: optional precomputed matrices Returns: Xk: optimal state trajectory Uk: optimal input trajectory phi: optimal cost status: solver status matrices: QP matrices """# Check argumentsifnot(4<=len([model,constraint,penalty,terminal,matrices])<=5):raiseValueError("Wrong number of arguments")# Build matrices if not suppliedifmatricesisNone:matrices=buildmatrices(model,constraint,penalty,terminal)# Get sizesnumx=model.B.shape[0]numu=model.B.shape[1]N=model.NnumVar=N*(numx+numu)+numx# Update initial conditionmatrices['lb'][0:numx]=model.x0matrices['ub'][0:numx]=model.x0# Get vectors to extract x and uallinds=np.mod(np.arange(numVar),numx+numu)xinds=allinds<numxuinds=allinds>=numx# Setup QP problemH=0.5*(matrices['H']+matrices['H'].T)# Make exactly symmetricdefobjective(x):return0.5*x.T@H@x+matrices['f'].T@xdefconstraint_eq(x):returnmatrices['Aeq']@x-matrices['beq']defconstraint_ineq(x):returnmatrices['blt']-matrices['Alt']@xbounds=list(zip(matrices['lb'],matrices['ub']))# Initial guessx0=np.zeros(numVar)# Solve QPwithwarnings.catch_warnings():warnings.simplefilter("ignore")result=minimize(objective,x0,method='SLSQP',bounds=bounds,constraints=[{'type':'eq','fun':constraint_eq},{'type':'ineq','fun':constraint_ineq}],options={'disp':False})# Process resultsstatus={'solver':'SLSQP','flag':result.status}status['optimal']=result.successifstatus['optimal']:X=result.xphi=result.funelse:X=np.nan*np.ones(numVar)phi=np.nan# Extract x and u trajectoriesXk=X[xinds].reshape((numx,N+1),order='F')Uk=X[uinds].reshape((numu,N),order='F')returnXk,Uk,phi,status,matricesdefbuildmatrices(model,constraint,penalty,terminal):"""Helper function to build QP matrices"""N=model.NA=model.AifA.shape[0]!=A.shape[1]:raiseValueError('model.A must be square')numx=A.shape[0]B=model.Bnumu=B.shape[1]ifhasattr(constraint,'G'):G=constraint.GH=constraint.Hpsi=constraint.psielse:G=np.zeros((0,numx))H=np.zeros((0,numu))psi=np.zeros((0,1))Q=penalty.QR=penalty.RP=penalty.PlittleH=sparse.block_diag([sparse.csr_matrix(Q),sparse.csr_matrix(R)])bigH=sparse.kron(sparse.eye(N),littleH)bigH=sparse.block_diag([bigH,sparse.csr_matrix(P)])bigf=np.zeros(bigH.shape[0])littleAeq1=sparse.hstack([sparse.csr_matrix(A),sparse.csr_matrix(B)])littleAeq2=sparse.hstack([-sparse.eye(A.shape[0]),sparse.csr_matrix(B.shape)])bigAeq=(sparse.kron(sparse.eye(N+1),littleAeq1)+sparse.kron(sparse.diags(np.ones(N),1),littleAeq2)).tocsr()bigAeq=bigAeq[:-numx,:-numu]bigbeq=np.zeros(numx*N)littleAlt1=sparse.hstack([sparse.csr_matrix(G),sparse.csr_matrix(H)])littleAlt2=sparse.hstack([sparse.csr_matrix(G.shape),sparse.csr_matrix(G.shape)])bigAlt=(sparse.kron(sparse.eye(N+1),littleAlt1)+sparse.kron(sparse.diags(np.ones(N),1),littleAlt2)).tocsr()bigAlt=bigAlt[:-littleAlt1.shape[0],:-numu]bigblt=np.tile(psi,N)numVar=len(bigf)LB=-np.inf*np.ones(numVar)UB=np.inf*np.ones(numVar)ifisinstance(terminal,dict)andall(kinterminalforkin['A','b']):Af=terminal['A']bf=terminal['b']bigAlt=sparse.vstack([bigAlt,sparse.hstack([sparse.csr_matrix((Af.shape[0],numVar-numx)),sparse.csr_matrix(Af)])])bigblt=np.concatenate([bigblt,np.asarray(bf).flatten()])elifisinstance(terminal,np.ndarray)andlen(terminal)==numx:LB[-numx:]=terminalUB[-numx:]=terminalelifterminalisNone:passelse:raiseValueError('Invalid terminal constraint')matrices={'H':bigH,'f':bigf,'Aeq':bigAeq,'beq':bigbeq,'Alt':bigAlt,'blt':bigblt,'lb':LB,'ub':UB}returnmatrices

# Exercise "Terminal penalty with and without terminal constraint"# [depends] functions/linearmpc.pyimportsysimportnumpyasnpfromcontrolimportdlqrfromtypesimportSimpleNamespacesys.path.append('functions/')fromfindXnimportfindXnfromlinearmpcimportlinearmpc# Define model, cost function, and bounds.A=np.array([[2.0,1.0],[0.0,2.0]])B=np.array([[1.0,0.0],[0.0,1.0]])N=3alpha=1e-5Q=alpha*np.eye(2)R=np.eye(2)# Bounds on variables.xlb=np.array([-15.0,-np.inf])xub=np.array([15.0,np.inf])ulb=np.array([-5.0,-5.0])uub=np.array([5.0,5.0])# Find LQR.K,P,_=dlqr(A,B,Q,R)K=-K# Sign convention.# Also calculate the control law with increased penalty.defriciter(A,B,Q,R,P):P=Q+A.T@P@A-A.T@P@B@np.linalg.solve(B.T@P@B+R,B.T@P@A)K=-np.linalg.solve(B.T@P@B+R,B.T@P@A)returnP,KP3=3*Pforiinrange(N):P3,K3=riciter(A,B,Q,R,P3)# Calculate Xn and Xf (maximum LQR-invariant set) using normal penalty.Xn,V,Z=findXn(A,B,K,N,xlb,xub,ulb,uub,'lqr',doplot=False)# Also calculate Xf using increased penalty (N=0 gives just Xf).Xn3,V3,_=findXn(A,B,K3,0,xlb,xub,ulb,uub,'lqr',doplot=False)# Set up MPC model/constraint/penalty objects.model=SimpleNamespace(A=A,B=B,N=N)constraint=SimpleNamespace(**Z)penalty=SimpleNamespace(Q=Q,R=R,P=P)terminal1=Xn[0]# Terminal set with normal penalty.terminal3=Xn3[0]# Terminal set with increased penalty.# Remove terminal constraint and check if MPC is still stabilizing.x1g,x2g=np.meshgrid(np.linspace(-10,10,25),np.linspace(-5,5,25))x0=np.vstack([x1g.ravel(),x2g.ravel()])Npts=x0.shape[1]Nstab=10# Steps to try before declaring stabilizing.Ps=[P,P3]names=['one','three']Xf_list=[terminal1,terminal3]x0stabilizing={}terminal=None# Remove terminal constraint.forninrange(len(names)):stab=np.zeros(Npts,dtype=bool)penalty.P=Ps[n]mpcmats=None# Rebuild matrices for new penalty.foriinrange(Npts):model.x0=x0[:,i].copy()forkinrange(Nstab+1):# If inside Xf, trajectory is stabilized.ifnp.all(Xf_list[n]['A']@model.x0<=Xf_list[n]['b'].flatten()):stab[i]=Truebreakifk==Nstab:breakxk,uk,_,status,mpcmats=linearmpc(model,constraint,penalty,terminal,mpcmats)ifnotstatus['optimal']:breakmodel.x0=xk[:,1]x0stabilizing[names[n]]=x0[:,stab]# Check where MPC gives the infinite-horizon control law.x1g,x2g=np.meshgrid(np.linspace(-10,10,50),np.linspace(-5,5,50))x0=np.vstack([x1g.ravel(),x2g.ravel()])X3=Xn[-1]# Feasible set.x0=x0[:,np.all(X3['A']@x0<=X3['b'].reshape(-1,1),axis=0)]Npts=x0.shape[1]infhorizon=np.zeros(Npts,dtype=bool)terminal=terminal1# Use original terminal set.penalty.P=Pmpcmats=Noneforiinrange(Npts):model.x0=x0[:,i]xk,uk,_,status,mpcmats=linearmpc(model,constraint,penalty,terminal,mpcmats)ifstatus['optimal']:infhorizon[i]=np.all(terminal['A']@xk[:,-1]<terminal['b'].flatten()-1e-5)x0infhorizon=x0[:,infhorizon]# Save data files.pa=V[0].T# Xf vertices (Mx2)pb=V[-1].T# X_N vertices (Mx2)pe=x0infhorizon.T# inf-horizon control law points (Kx2)pg=x0stabilizing['one'].T# stabilizing with P (Kx2)pf=x0stabilizing['three'].T# stabilizing with 3P (Kx2)withopen('NoTerminal.dat','w')asf:forlabel,datain[('pa',pa),('pb',pb),('pe',pe),('pg',pg),('pf',pf)]:f.write(f'# {label}\n')np.savetxt(f,data,fmt='%.6f')f.write('\n\n')